数字引领时代 智能开创未来

学院首页

图片新闻

学院新闻

快速通道

精彩影像

媒体报道

学院概况

学院介绍

学院领导

机构设置

学术组织

师资力量

教师一览

教授

副教授

讲师

特聘教授

行政及教辅人员

科学研究

科研机构

商务大数据研究中心

商务信息实验室

上海对外经贸大学环球...

海关总署全球贸易监测...

金融大数据与精算科学...

科研项目

科研成果

发表论文

著作参编书籍

科研获奖

学术活动

学术会议

人才培养

本科生教育

专业设置

各系介绍

课程建设

培养方案

分级教学

规章制度

研究生教育

专业介绍

培养方案

导师队伍

规章制度

质量报告

国际化办学

招生就业

本科生招生

专业设置

硕士生招生

招生工作

专业介绍

导师队伍

博士生招生

招生工作

专业介绍

导师队伍

实习就业

实习基地

就业工作

党务工作

组织结构

党建活动

学生工作

团学天地

新闻动态

学生组织

品牌活动

数说党史 数说中国

计算机文化节

数学文化节

中国大学生数学建模竞...

美国大学生数学建模竞...

“访万企,读中国”社...

统信大讲堂

实践项目

“水滴”志愿者项目

“高数帮帮站”活动

创新创业项目

学子风采

学生事务相关文件及通...

内部登录

内部通知

会议室日程

学院文件

联系我们

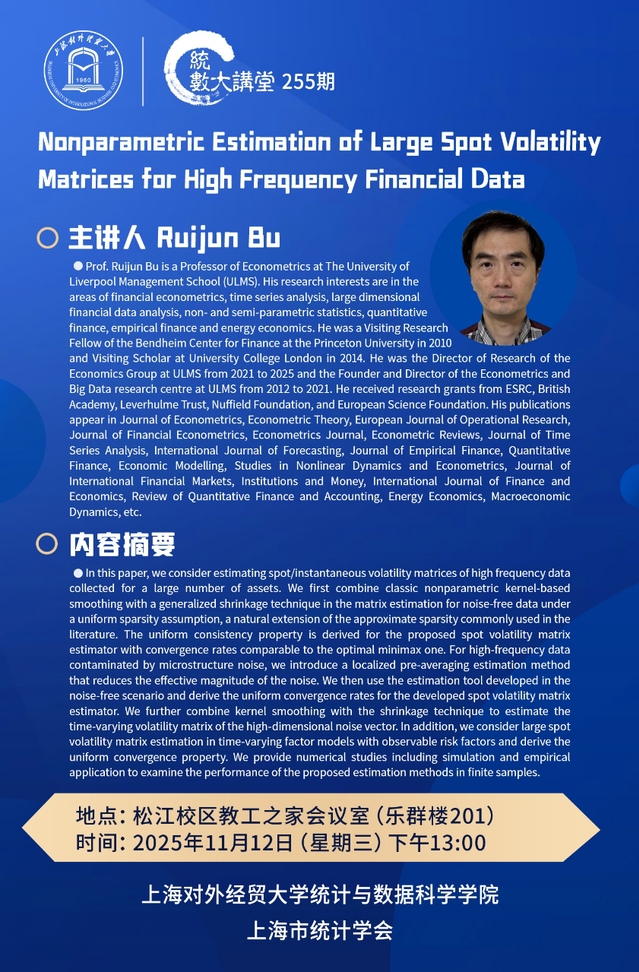

11.12 255 Nonparametric Estimation of Large Spot Volatility Matrices for High Frequency Financial Data